RYANAIR REPORTS STRONG HALF YEAR PROFITS OF €2.18BN DUE TO RECORD SUMMER TRAFFIC

H1 highlights:

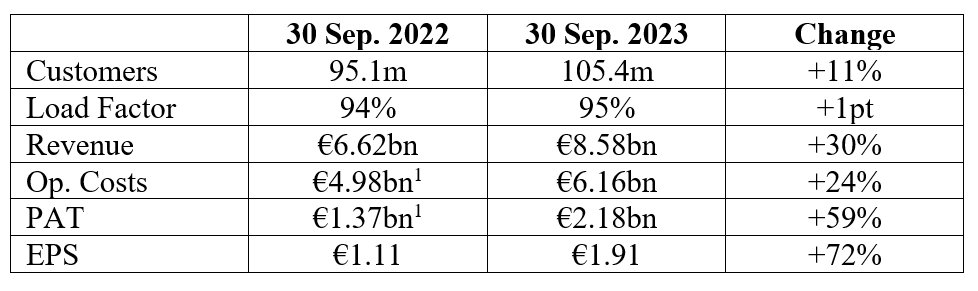

Traffic grew 11% to 105.4m (95% load factor).

Rev. per pax +17% (ave. fares +24% & ancil. rev. +3%).

3 new bases & 194 new routes in S.23.

124x B737 “Gamechangers”. Total fleet of 563 aircraft at 30 Sep.

Fuel bill rose €0.6bn (+29%) to €2.8bn.

Fuel hedging extended – c.85% FY24 at $89bbl & over 50% FY25 at $79bbl.

Net cash of €0.84bn (31 Mar. €0.56bn), over €1bn debt repaid.

300x Boeing MAX-10 order underpins growth decade to 300m pax p.a. by FY34.

€400m maiden div. & div. policy announced.

Ryanair’s Michael O’Leary, said:

ENVIRONMENT:

“Ryanair is one of the most environmentally efficient major EU airlines. With a young fleet and high load factors, our CO2 per pax/km is just 65 grams. We invest heavily in new, more efficient, technology. In H1 we took delivery of 26, new, B737-8200 “Gamechangers” (4% more seats, 16% less fuel & CO2). We’re accelerating the retro-fit of scimitar winglets to almost 130 B737NGs (target 409 by 2026), reducing fuel burn by 1.5% and lowering noise emissions by a further 6%. We are working with fuel partners to accelerate SAF supply and are on track to achieve the Group’s ambitious 2030 goal of powering 12.5% of Ryanair flights with SAF (9.5% already secured).

ADVERTISEMENT

The urgent reform of Europe’s inefficient ATC system is one of the most significant environmental initiatives the EU can deliver. In 2023, French ATC has (so far) inflicted over 60 days of strikes on our sector, during which the French Govt. use minimum service laws to protect local/domestic flights while disproportionately cancelling overflights. In Sep., we delivered a petition (signed by 1.5m customers) calling on the EC to protect the single market for air travel by protecting overflights (while respecting ATC Unions right to strike), as is already the case in Greece, Italy and Spain. Sadly, we have yet to see any action from President Ursula von der Leyen on this key environmental initiative.

Our recent order for 300 Boeing MAX-10 aircraft (21% more seats, 20% less fuel & CO2 and 50% quieter), enabled us to reset the Group’s environmental targets as we strive to more sustainably grow traffic to 300m p.a. by FY34. In H1, we set a very ambitious target of 50 grams of CO2 per pax/km by FY31 (previously 60 grams by FY30) and published Ryanair’s 1.5 degree Climate Transition Plan.

SOCIAL:

We expect to create over 10,000 new, well-paid, jobs for highly trained aviation professionals as the Group expands our fleet to 800 aircraft by FY34. Building on the success of our aviation training facilities in Dublin, Stansted, Bergamo and East Midlands, we’re opening 2 new excellence centres in Krakow and Madrid to accelerate local crew training and development in those major markets. Our recently announced engineering academy will support 1,000 apprentices annually as we train the next generation of highly skilled mechanics and engineers. Ryanair Labs is also growing at its dev. hubs in Dublin, Madrid, Portugal and Wroclaw to support Ryanair’s customer service, our efficiency and scalability over the coming decade.

Ryanair’s investment in resilience ahead of our S.23 schedule (increased crew ratios, doubling the capacity of our Dublin and Warsaw ops centres, enhanced day-of-travel app. and continuously improving live customer comms.) ensured that our passengers and crews could enjoy Ryanair’s industry leading OTP and reliability, despite significant ATC disruptions this year. This is reflected in our strong H1 CSAT score of 84%, notwithstanding over 60 days of French ATC strikes.

GROWTH & FLEET:

During S.23 we operated our largest ever schedule, including 3 new bases and over 190 new routes. We delivered record traffic across peak summer months. This winter we’ll operate 6 new bases (Athens, Belfast, Copenhagen, Girona, Lanzarote & Tenerife), and over 60 new routes including our first 17 routes to Albania. To date over 90% of S.24 capacity is already on sale, including over 180 new routes.

While Boeing are currently suffering delivery delays with Spirit (their fuselage supplier), we are working with them to minimise delays ahead of peak S.24. At this stage, we are concerned that up to 10 of our 57 contracted Gamechanger deliveries pre S.24 may be delayed until winter 2024.

We expect European airlines will continue to consolidate over the next 2-3 years, with the takeover of ITA (Italy) and the sale of TAP (Portugal) and SAS (Scandinavia) already underway. While Pratt & Whitney engine (GTF) issues and inspection programme threaten to substantially curtail competitor and lessor capacity between 2024 and 2026, the large backlog of OEM aircraft deliveries is also likely to constrain capacity in Europe for the next 3 or 4 years. These capacity constraints, combined with our widening cost advantage, our judicious fuel hedging, strong balance sheet, low-cost aircraft orders and industry leading operational resilience, creates significant traffic and profit growth opportunities for Ryanair as we expand to carry 300m pax p.a. by FY34.

H1 FY24 BUSINESS REVIEW:

Revenue & Costs

H1 scheduled revenues increased 37% to €6.1bn. Traffic grew 11% to 105.4m while ave. fares rose 24% to c.€58 due to a strong Easter and record S.23 demand. Ancillary revenue increased 14% to €2.5bn (c.€23.70 per passenger). Total H1 FY24 revenue therefore rose 30% to €8.6bn. Total operating costs increased 24% to €6.2bn, primarily due to much higher fuel costs (+29% to €2.8bn), higher staff costs (reflecting pay restoration, pre-agreed pay increases and higher crewing ratios as we invested in ops. resilience) and higher ATC fees (incl. airport & handling charges). Ryanair’s cost advantage over most of its EU competitors continues to widen, with H1 ex-fuel unit costs finishing just under €32.

Our FY24 fuel requirements are almost 85% hedged at approx. $89bbl (a mix of forwards and caps) while our FY25 hedging has increased to just over 50% at approx. $79bbl. This will deliver savings of approx. €300m on the fuel already hedged for FY25. Over 90% of FY24 €/$ opex is hedged at 1.08 and almost 50% of FY25 is hedged at 1.12. This strong hedge position leaves us very well protected from recent short term fuel price volatility which many competitors are more, or fully, exposed to.