Amadeus: Asia leads rapidly expanding global aviation market

New analysis from Amadeus Air Traffic Travel Intelligence solution reveals that worldwide air traffic volume grew five per cent between 2011 and 2012, with Asia being the largest, fastest-growing and most competitive market for air travel.

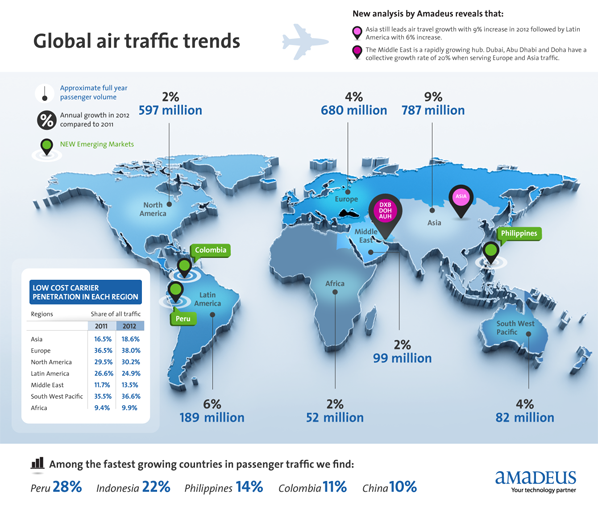

The solution - which provides comprehensive passenger volume data, including both direct and indirect sales of airline seats - shows that Asia experienced year over year growth of nine per cent between 2011 and 2012, followed by Latin America, at six per cent.

The tool, part of the Amadeus’ Travel Intelligence portfolio, calculates the most accurate air passenger volume for any origin and destination worldwide.

Among other key findings, the study reveals that 22 per cent of all global air travel is concentrated on just 300 origin and destination ‘super routes ’, each of which carries over one million passengers annually.

Furthermore, 69 per cent of all global air travel is made on major routes with 100 thousand annual passengers.

In terms of connecting air traffic, the analysis shows the Middle East as a strong performer, with the three key airports of Doha, Abu Dhabi and Dubai all showing high connecting traffic volumes.

For instance, when taken as a group the three airports now serve roughly 15 per cent of all air traffic volume that goes from Asia to Europe and from Europe to the South West Pacific.

Furthermore, Europe-Asia traffic routed via the Middle East is growing at roughly 20 per cent per annum.

The analysis also shows Asia as the market with the highest airline competition, 75 per cent of the region’s air traffic is operated by three or more airlines and 27 per cent by five or more airlines, making this a region with a very intense competition in all its air travel routes.

This contrasts sharply with other regions such as the Middle East and Europe where just half of all air traffic on its routes is operated by three or more airlines.

Analysis of the busiest routes in the world by passenger volume shows that seven out of the top ten world’s busiest air travel routes are in Asia.

Jeju-Seoul in South Korea remains the world’s busiest air route, and many of 2011’s top origin and destination routes return to the league table for 2012, however, there has been some change: in particular, Beijing-Shanghai has risen from seventh-busiest route in the world in 2011, to fourth-busiest in 2012.

Sapporo-Tokyo has overtaken Rio de Janeiro-Sao Paulo to second-busiest route ranking, and Okinawa-Tokyo has entered the top ten, as ninth-busiest route in the world.

Some 35 per cent of air travel in Europe and North America is made on smaller routes with fewer than 100 thousand annual passengers.

This contrasts sharply with other regions such as Asia where 85 per cent of air travel is concentrated on routes that carry over 100 thousand passengers each year.

This concentration of Asian air travel suggests the region’s growth may continue as there is an opportunity for airlines to develop secondary links beyond the heavily competitive super routes.

In addition, the analysis shows that in Asia, the larger routes with over 100 thousand annual passengers have a four to nine per cent growth range, but the smaller and medium sized routes in the region are growing at approximately 19-21 per cent per annum.

Globally, the airline industry has become consistently more competitive over the past three years.

The percentage of air traffic served by just one or two airlines has fallen by two per cent each year from 39 per cent in 2010 to 35 per cent in 2012.

Concurrently, the percentage of air traffic with four or more competing airlines has also risen consistently from 35 per cent in 2010 to 38 per cent in 2012.

Asia is the market with the highest competition between airlines in the world, with three quarters of air traffic volume served by more than three airlines and only a quarter of air traffic served by one or two airlines.

This contrasts strongly with other regions, for example in Europe 45 per cent of air traffic volume is served by just one or two different airlines and in the Middle East 50 per cent of all air traffic has only one or two competing carriers.

The highly competitive nature of air travel in Asia may be due to the high concentration of passengers on a relatively low number of ‘super routes’, where several airlines vie for dominance.

The rise of low cost airlines has been significant over the past decade, but this has been largely limited to traditional markets.

Today, Europe has the highest concentration of LCC traffic, representing 38 per cent of total air travel in 2012.

The South West Pacific and North America regions also have significant LCC penetration, with 37 per cent and 30 per cent respectively.

However, in markets where air travel is growing most strongly, LCCs’ respective share of overall air travel remains at modest levels – in the Middle East LCCs represent just 14 per cent of all air travel, in Asia 19 per cent and Latin America 25 per cent.

Within specific regions, the spread of LCCs varies strongly.

In Europe, Spain has the highest share of departing LCC traffic at 57 per cent, followed by the UK where 52 per cent of all originating air travel is now made on low cost airlines, up four per cent from 2011 and passing the 50 per cent milestone for the first time.

Despite the low overall share of low cost air travel in Asia, some countries have bucked this trend, for example 65 per cent of all air travel in the Philippines and 61 per cent of all air travel in Thailand is made on low cost carriers.

The region’s three key airports of Dubai, Doha and Abu Dhabi, are all experiencing strong overall air traffic growth of around ten per cent per annum and they have very high levels of connecting traffic, with each airport seeing around 50 per cent of its total air travel volume connect.

These figures demonstrate the region’s increasingly important role as a hub between Europe and the emerging markets of Asia and the South West Pacific.

When the three airports are taken as a group they already serve around 15 per cent of air traffic volume between Asia - Europe and Europe - South West Pacific.

It is particularly interesting to note that overall traffic volume between Europe and Asia is growing by approximately seven per cent year over year, but traffic volume between these two locations and routed via the Middle East grew by approximately 20 per cent between 2011 and 2012.

Pascal Clement, Head of travel intelligence, Amadeus, commented: “The rapid pace of change and increasing competitiveness of the global airline industry, as evidenced by this data, means airlines and the wider travel industry increasingly need to base operational decision-making on data insights and analytics, in order to identify opportunities and risks as they emerge.”

He continued: “This data provides good news for the airline industry, showing that passenger air traffic has increased in every region of the world from 2011 to 2012.

“As in 2011, this growth is led by Asia, however, the data points to a further opportunity in the region, where the majority of traffic is on a small number of busy routes.

“The Amadeus Air Traffic solution helps airlines plan and develop networks that respond to true passenger traffic and meet a clear need in the market based on complete O&D data.”