End of an Era for lastminute.com

By Anna Gouldman

Online consolidation continues as last week saw Sabre’s Travelocity Europe complete its acquisition of lastminute.com, marking the end of an era for many internet-savvy travellers. Sabre expects the addition of lastminute.com to improve its position in the European marketplace.

Online consolidation continues as last week saw Sabre’s Travelocity Europe complete its acquisition of lastminute.com, marking the end of an era for many internet-savvy travellers. Sabre expects the addition of lastminute.com to improve its position in the European marketplace.

The lastminute.com acquisition, valued at £577 million, gives Sabre Europe’s leading travel company, with 2,000 employees in 14 countries.

The combined force of lastminute.com and Travelocity will mean fierce competition for IAC’s Expedia and Cendant.

Sabre believe this move places them at a competitive advantage because they are now penetrating all key channels of travel online and offline around the world, demonstrating their key objective: “Connecting People to the greatest travel possibilities”.

A Sabre spokesperson told BTN: “We don’t own specific suppliers and are well-positioned in all the markets in which we participate”.

ADVERTISEMENT

Commenting on Sabre’s dependency on the continued support of its GDS, Travel Consultant, Marty Gast, who helped launch Travelocity in 1996, commented: “This acquisition ensures that lastminute.com will funnel international travel through the Sabre GDS and prevent another GDS from obtaining those reservations”.

Commenting on Sabre’s dependency on the continued support of its GDS, Travel Consultant, Marty Gast, who helped launch Travelocity in 1996, commented: “This acquisition ensures that lastminute.com will funnel international travel through the Sabre GDS and prevent another GDS from obtaining those reservations”.

A 2005 PhoCusWright report estimated the combined share of lastminute.com and Travelocity Europe made up 28% of online travel in Europe in 2004.

Michael Cannizzaro, Director of Information Services, PhoCusWright Inc., believes the acquisition puts Sabre firmly in the lead among online travel agencies in Europe and will also benefit other international operations. He commented: “Assuming LMIN integration issues do not trump the expediency of acquired growth in Europe, the purchase also gives Sabre more leeway to concentrate on ventures in Asia”.

Michael Cannizzaro, Director of Information Services, PhoCusWright Inc., believes the acquisition puts Sabre firmly in the lead among online travel agencies in Europe and will also benefit other international operations. He commented: “Assuming LMIN integration issues do not trump the expediency of acquired growth in Europe, the purchase also gives Sabre more leeway to concentrate on ventures in Asia”.

He believes Priceline and Ctrip could be next to be snapped up, commenting: “Where they ultimately fit in the conglomerate landscape I could not say, but most likely it will not be by themselves”.

Offering his predictions for the online arena, Michael commented: “While there will always be niches filled and new needs addressed by technology, the pattern appears to be that the big players will then move to fill those needs after smaller entities begin to address them”. He added: “Witness the moves by the US’s big three to develop user-defined content and the application of datamining techniques to real time pitches to site visitors”.

![]() According to PhoCusWright projections, in the U.S., leisure/unmanaged business online gross bookings are projected to increase by nearly 50% from 2004 to 2006, to $78.5 billion. Corporate online gross bookings are expected to grow at an even faster pace, at around 57%, from 2004 to 2006 to reach $36.5 billion. In Europe, leisure/unmanaged

According to PhoCusWright projections, in the U.S., leisure/unmanaged business online gross bookings are projected to increase by nearly 50% from 2004 to 2006, to $78.5 billion. Corporate online gross bookings are expected to grow at an even faster pace, at around 57%, from 2004 to 2006 to reach $36.5 billion. In Europe, leisure/unmanaged

business online gross bookings are expected to more than double from 2004 to

2006 to €41.6 billion.

In an industry that is projected to double its bookings over the next 2 years whilst becoming rapidly dominated by a conglomerate landscape, BTN asked lastminute.com why they decided this was the right time accept a takeover. A spokesperson responded: “lastminute.com evaluated the strategic and cultural fit and determined that Travelocity shared the same values and vision as lastminute.com”.

Brent Hoberman will take up position as CEO of the combined lastminute.com and Travelocity European operations, reporting to Michelle Peluso. Damon Tassone, currently president of Travelocity Europe, will become deputy CEO.

Brent Hoberman will take up position as CEO of the combined lastminute.com and Travelocity European operations, reporting to Michelle Peluso. Damon Tassone, currently president of Travelocity Europe, will become deputy CEO.

Unphased by the concept of becoming a managed company, lastminute.com stated: “The business looks forward to growing and developing as part of Travelocity Europe and Sabre Holdings”.

lastminute.com’s offices will remain in London, but plans have not yet been announced for the combined business moving forward.

Travelocity will re-evaluate its other brands in different markets. In an effort to maintain a broad online presence, it is expected that multiple brands will continue to operate.

A lastminute.com spokesperson revealed: “Regardless of the way the combined company will be structured, Travelocity intends to position lastminute.com as the lead brand in most of the countries in which it operates”.

lasminute.com expects its product offering will be strengthened, with the anticipated offering of travelocity’s 20,000-strong net rate hotel program to lastminute.com customers as early as autumn 2005.

One of the priorities for the merger will be cost savings and product sharing opportunities. lastminute.com’s last annual report revealed losses almost doubled in the year to september 2004 to £77.2m ($143.5m), from £47.7m in 2003 despite higher turnover.

Shares during its last trade on the London Stock Exchange were at £1.65.

A lastminute.com spokesperson revealed: “we expect cost-savings and revenue synergies to stem from a wide range of sources. These include leveraging new supplier relationships, centralising operations and administrative functions, streamlining marketing spend across brands, consolidating platforms and sharing technologies”.

I am told that customers and industry partners have reacted positively to the move.

Whilst this acquisition marks the end of an era for a company that survived the dotcom boom and bust, the deal represents a new beginning for lastminute.com, as the crucial jigsaw piece, that advances Sabre into a strong position in the international online travel arena.

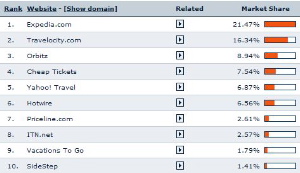

Top 10 Travel Agency sites in the US by market share of visits, June 2005, Source Hitwise

Top 10 Travel Agency sites in the UK by market share of visits, June 2005, Source Hitwise

——-